Let’s face it – we all know our net income is a whole lot less after the Canada Revenue Agency takes its piece of the pie. Part of that loss concerns payroll deduction remittances in Canada.

As an employee, you want a breakdown of Revenue Canada payroll deductions and as a business owner, HR payroll specialist, bookkeeper, or accountant, you need to explain those deductions to your employees and clients.

There’s no doubt explaining payroll deductions can be a challenge, but along with that, calculating deductions, and knowing how to remit those deductions to the government – can be complicated as well.

In this blog post, we will walk you through everything you’ll need to know about payroll remittances in Canada.

Here’s exactly what we’ll be covering:

While some people use the terms deduction and remittance interchangeably, a deduction is the amount taken from the employee’s pay for Canada Pension Plan (CPP), Employment Insurance (EI) and income tax deductions.

The remittance to the government includes the employee’s CPP, EI and income tax deductions plus the employer’s CPP and EI contribution for that employee.

When it comes to payroll deductions, if you’re an employer, you must calculate and deduct:

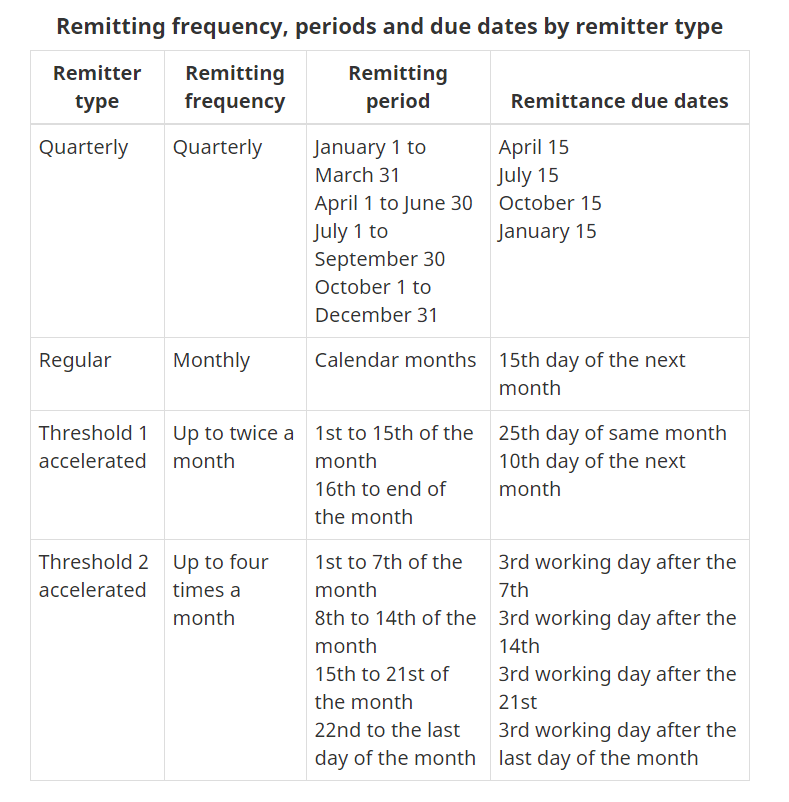

These are employers who do not qualify to remit quarterly as a new small employer. They are considered regular remitters if their average monthly withholding amount (AMWA) two years ago was less than $25,000, and the CRA has not advised them to remit at a different frequency.

If you’re a regular remitter, the CRA must receive deductions on or before the 15th of the month after the month employees were paid.

These new small employers with a monthly withholding amount of zero to $999.99, a perfect compliance history, and an account that has been open for 12 months or longer.

The CRA must receive the remittance on or before the 15th day of the month immediately following the end of each quarter (in plain English – April 15, July 15, October 15, January 15).

This is an employer with an average monthly withholding amount of $25,000 to $99,999.99 two calendar years ago.

For wages paid in the first 15 days of the month, remittances are due by the 25th day of the same month.

For wages paid from the 16th to the end of the month, remittances are due by the 10th day of the following month.

This is an employer with an average monthly withholding amount of $100,000 or more, two calendar years ago.

If you fall in this category, remit through a Canadian financial institution so that CRA receives them within three working days following the last day of the following pay periods:

Here’s a great visual by the CRA that gives you everything we just covered in a table format.

The CRA’s own payroll deductions online calculator can be used to calculate federal, provincial (except for Quebec) and territorial payroll deductions.

CRA notes “The reliability of the calculations produced depends on the accuracy of the information you provide.”

Be aware that there is actually no such thing as a payroll remittance calculator because the remittance is THE total amount you send to the CRA after calculating the payroll deductions for each employee.

Here is a list of province specific calculators you can use:

However, if your head office is in one province and your employee(s) report to a regional office in a different province, you pay tax based on where they report or the office from which they are paid.

The CRA provides five helpful examples here to help you figure out which province or territories payroll deductions table you should be using for your employees.

We’re talking money and government so of course there is a payroll deductions form to fill out – actually make that two TD1 forms – the federal form and the provincial form.

The TD1 Personal Tax Credits Return determines the amount of tax to be deducted from an individual’s employment income, or other income, such as pension income.

Your employees fill out the forms and give them to you. As the employer or payer, you keep the completed forms with their records – do NOT send the TD1 forms to the CRA!

You will need to provide your account or BN number and the amount you are paying.

You will need to order a payroll remittance form or remittance voucher because it provides CRA with specific account information and has to be submitted with every payment.

Plan ahead because it takes 5 to 10 business days to receive the payroll remittance forms by mail after placing an online or phone order.

You will find at least one payroll remittance form sample and many more on this CRA page.

If you need help, the CRA offers step by step instructions for employers and their representatives here.

You can submit your payroll remittance online using online banking via your financial institution, you can pay with Visa Debit, Debit Mastercard or Interac Online and pre-authorized debit. You can also pay using a credit card, PayPal, Interac e-Transfer and by cheque.

Even when you rely on a payroll software or outsource payroll deductions and remittances to a payroll specialist, you should be aware of the basics.

Get the facts from trusted experts such as bookkeepers and accountants, but you can also start with the CRA’s own Employers’ Guide Payroll Deductions and Remittances.

Just so you, that guide runs 68 pages!

We’d mentioned the importance of timely remittances earlier.

How seriously does the CRA takes its remittance dates?

In the 68-page guide, the remittance due dates chart is just a page or two after the title page/cover and BEFORE the table of contents. Check out this ‘submit by this’ date table.

Scroll through the 68 pages, check out the many links provided to give you more detail, and you may reconsider your DIY approach to payroll, particularly when you see the Penalties, Interest and other Consequences chapter that starts on page 11 of 68.

CRA can and will levy penalties and interest and even these get a little complicated.

If you don’t deduct CPP, EI and income tax – CRA will penalize your company 10% the first time and 20% if you do it twice in the same year.

Penalties – late or failure to remit:

Here’s what you should know about interest:

As far as the CRA is concerned, it’s your job and your responsibility to really understand the rules and regulations.

The CRA fully expects you to stay on top of everything from CRA updates and changes to due dates that fall on a national statutory holiday or right in the middle of your long-awaited vacation.

Remember – it is not your employees’ money or your company’s money – it is the CRA’s money and you’re holding it in trust for them.

So, what can you do to avoid penalties and interest?

If you really must do-it-yourself:

If you’ve read the blog this far and you’re feeling a little overwhelmed then outsourcing your payroll remittances and deductions might be the route for you.

Here are some reasons why outsourcing might be a better option:

If any of the points above ring true for you, then be sure to check out our flagship payroll software and get all your payroll deductions/remittances calculated for you!

In the evolving Canadian labor market of 2026, the distinction between a contractor vs employee…

There was a moment, somewhere between 2012 and 2015, when Canadian employers quietly lost control…

What started as a viral TikTok trend has arrived at the legislature. Here is what…

March 3rd has a specific feeling You know the one. It's not quite relief. It's not quite exhaustion. It's that particular fog that settles in…

If you run a Canadian business with 10–50 employees, payroll probably feels routine. You approve…

Cyberattacks aren’t just targeting massive tech companies anymore. They’re targeting small and mid-sized businesses, and…

{kind=link}

{kind=link}